Contents

Contents

After several years of lower valuations, tighter funding, and skepticism about the viability of many business models, the FinTech sector has entered a more demanding phase. Investors are looking more closely at operational performance: whether companies can capture new sources of value, turn technology into a lasting advantage, and navigate a more complex regulatory and geopolitical environment while expanding into new products and markets.

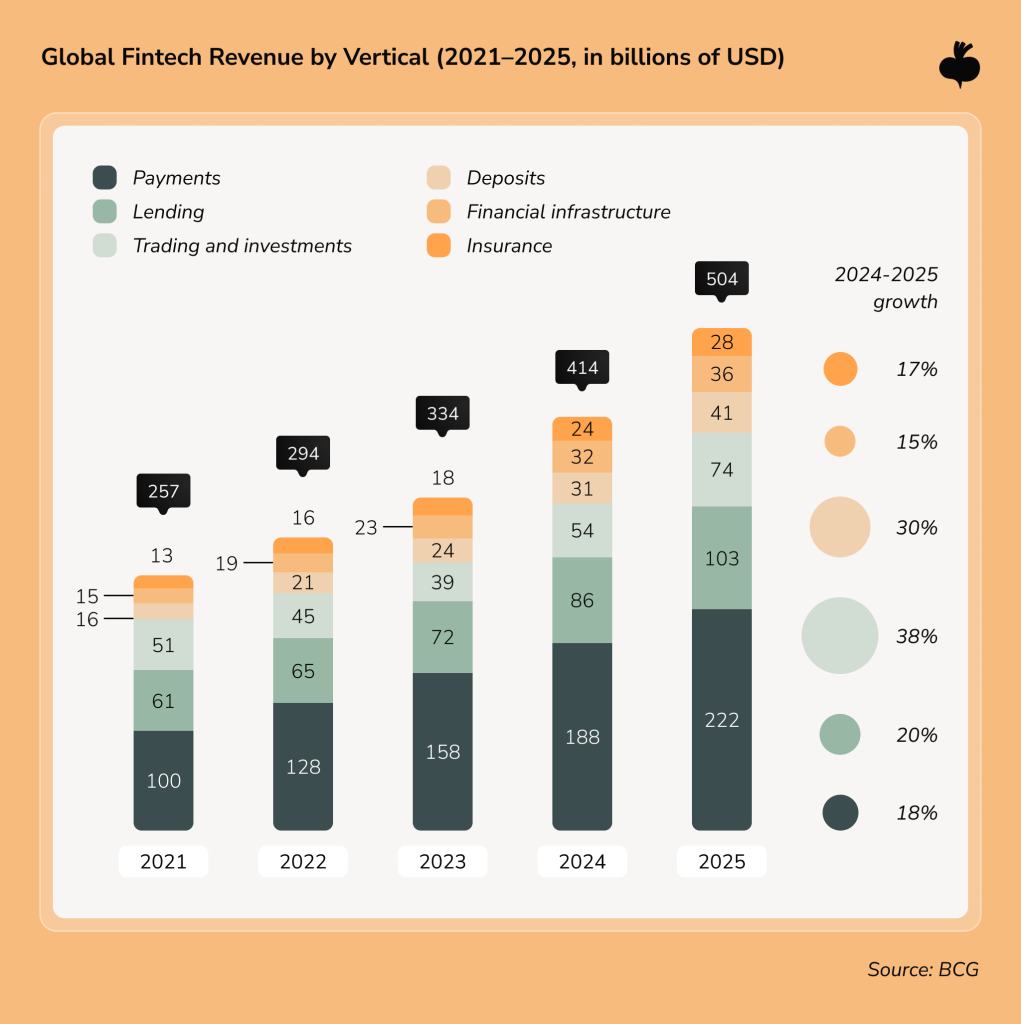

The numbers support that shift. The 2026 Global Fintech Report from FT Partners & BCG found that global fintech revenues surpassed $504 billion in 2025, growing more than four times as fast as traditional financial institutions. Among the largest public fintechs, the share of profitable companies rose to 74%, while average EBITDA margins climbed to 20%. Growth has returned, but so have public-market scrutiny, tighter regulation, and a higher bar for proving impact.

Below, we look at the FinTech industry trends most likely to create measurable business value over the next two years and the operational, regulatory, and technology drivers behind them.

The State Of FinTech In 2026: From Recovery to Sustainable Growth

According to the same FT Partners & BCG report, fintech now accounts for roughly 4% of the global financial services revenue pool, making it large enough to influence the sector while leaving substantial room for growth. The momentum comes from operating performance rather than cheap capital, and investors have grown selective. Late-stage funding grew sharply between 2023 and 2025 while seed-stage funding contracted — a sign that capital is concentrating around companies with proven economics.

Regulatory convergence is a second defining force. As BCG and FT Partners note, the gap between banks and fintechs is narrowing across the US, UK, and EU, with charter applications rising and compliance expectations climbing. Large incumbents are also actively investing in technology. JPMorgan Chase, for example, plans to spend roughly $20 billion annually on tech, moving AI from fraud detection and chatbots into revenue-generating banking products and operational workflows.

As large institutions modernize, the FinTech advantage in speed and user experience narrows, which pushes newer players toward niche innovation, partnerships, and infrastructure. The takeaway for leaders is that the future of FinTech will be decided by execution more than by the boldness of any single idea, and winners will be organizations that can translate a market shift into a reliable, well-engineered product.

Trend #1: AI in FinTech Trends Move Into Core Financial Operations

For the past two years, generative AI in FinTech mostly meant pilots: customer-facing chatbots and internal coding copilots. In 2026, the focus has shifted to how AI can directly change operational processes. The biggest near-term gains show up in software delivery, underwriting, compliance, fraud operations, and customer support, where results depend on redesigning the workflows.

Deloitte’s 2026 Financial Services Predictions point to a shift from using AI primarily for productivity toward investing in AI-native banking products built with AI at their core. The report estimates these offerings could generate up to $75 billion in incremental revenue for top US banks by 2030, while also highlighting growing adoption of agentic AI in wealth management and insurance.

AI maturity across financial services varies widely. Some companies have made AI core to finance, servicing, and fraud prevention, while others still use it for one-off tasks. For most, the best place to start is high-volume work where data is already available, such as reconciliation, KYC and AML checks, fraud monitoring, and first-line support. Custom AI solutions and AI assistants for financial services are already helping institutions reduce manual work by integrating with existing systems and supporting real operational workflows.

Trend #2: Embedded Finance Turns Software Into a Revenue Engine

Embedded finance opens a clearer path to new revenue streams by placing financial products directly inside non-financial customer journeys. This category can include embedded payments, digital wallets, lending offers, insurance products, or banking-as-a-service (BaaS) models. This market is projected to expand from around $115 billion in 2026 to more than $250 billion by 2030, at a compound annual growth rate of 22%.

The business logic is straightforward. Software companies can now embed financial actions into the customer workflows they already support, including payments, loans, insurance offers, or payouts. A SaaS accounting platform that already processes a merchant’s cash flow, for example, may be well-positioned to offer working-capital loans underwritten by that same data.

Yet the opportunity comes with a clear caution. The 2024 collapse of the BaaS provider Synapse, which locked more than 100,000 users out of over $265 million in deposits, showed what happens when ledger reconciliation and oversight are treated as afterthoughts.

Trend #3. Real-Time Payments Become A Competitive Baseline

Instant payment rails have crossed from novelty to expectation. In the US, the Federal Reserve’s FedNow service surpassed 1,700 participating financial institutions as of May 2026 and processed 2.73 million payments worth $271 billion in the first quarter alone.

Once funds move in seconds, instant settlement becomes table stakes, and the contest shifts to fraud prevention. There’s no longer an overnight window to catch suspicious transfers, so fraud models built for batch processing fall short. Deloitte’s 2026 banking outlook flags this directly, warning that financial crime risks are escalating, fueled by AI-enabled fraud, and that integrated, technology-driven defenses have become imperative.

The institutions that win here pair real-time rails with real-time risk scoring, account validation, and behavioral analytics that flag anomalies before a transaction becomes a customer problem.

Adopting a new rail is the visible step. Building the surrounding fraud, validation, and reconciliation layer is the work that actually protects margins and customers. It depends on modern data infrastructure that can process and act on transaction data the moment it arrives, a theme explored further in our look at when real-time data becomes a business advantage.

Trend #4: Open Banking Evolves Into Open Finance

Open banking gave customers the right to share their banking data with authorized third parties. Open finance extends that principle across the whole financial life, including savings, investments, pensions, and insurance, and it is the next structural shift worth watching.

The regulatory picture is uneven, which is exactly why it deserves attention. In the EU, the Financial Data Access (FiDA) regulation is expected to be adopted in 2026 and rolled out in phases from 2027 onward, covering mortgages, investments, pensions, and insurance.

The US is taking a different path. The CFPB finalized its Section 1033 personal financial data rights rule in late 2024, but enforcement and compliance timelines are now uncertain because of litigation and reconsideration. Consumer demand for connected financial experiences continues to pull the market forward regardless.

For decision-makers, the strategic implication is to build for data portability now rather than wait for final rules. Broader data sharing creates room for new services, including more accurate credit assessments, holistic financial dashboards, and faster switching between providers.

Organizations that turn shared data into useful products, rather than only compliant APIs, will capture the value. Among the future trends in fintech, open finance has one of the broadest implications for business models because it gives providers a fuller view of each customer’s financial life.

Trend #5: RegTech: Compliance Becomes A Technology Capability

Compliance is moving out of the back office and into the product. As regulations tighten and AI takes on more decisions, the expectation has shifted. Teams are no longer reviewing risk post factum — systems are expected to manage it continuously and explain themselves on demand.

The EU’s DORA framework, now in force, sets binding requirements for ICT risk management across the financial sector, including incident reporting and oversight of critical third-party providers. The EU AI Act classifies certain AI systems in finance and insurance as high-risk, requiring documented data governance and meaningful human oversight (although fraud detection is explicitly carved out of that specific high-risk category, it still falls under GDPR and supervisory expectations).

This is where RegTech matures from a point solution into an architecture layer. Modern compliance programs automate policy monitoring, sanctions screening, audit-trail generation, and regulatory reporting. Deloitte frames the broader challenge in its 2026 banking outlook, noting that many banks remain stuck in experimentation and need to treat AI as core infrastructure with governance and data quality at the center. Treated as infrastructure, compliance can reduce manual review, shorten market-entry work, and make audits easier to support.

As AI-enabled fraud and sanctions complexity increase, integrated, technology-driven defenses become a board-level priority and baseline requirement for organizations that want to scale across markets.

Trend #6: Customer Experience Becomes a FinTech Differentiator

As products converge and payment rails become more standardized, customer experience has a stronger influence on acquisition and retention. Customers increasingly expect financial services to feel as immediate and personalized as the best consumer apps, but many providers still fall short. J.P. Morgan reports that 65% of consumers expect frictionless payments, while only 45% of merchants prioritize one-click experiences.

The institutions pulling ahead use transaction and behavioral data to anticipate what customers need next: a relevant product, a better payment option, or a warning before a small issue becomes a bigger one. In wealth management, Deloitte expects agentic AI to deepen this shift, projecting that AI-driven automation could increase adviser productivity by 30 to 100% by 2032 and make personalized service easier to scale.

Conversational AI plays a growing role here. The lesson from the past two years is that poorly built scripted bots erode trust, while well-integrated assistants can improve resolution and reduce pressure on support teams. Getting there relies on predictive analytics solutions that turn raw activity signals into anticipation, an approach we discuss in how CX teams use predictive analytics.

What These FinTech Trends Mean for Industry Leaders

Read together, the biggest fintech trends of this cycle point in one direction. Value is shifting from novelty toward execution. A few priorities follow naturally for leaders deciding where to invest over 2026 and 2027.

- Invest where AI changes the workflow. Prioritize high-volume processes such as underwriting, reconciliation, servicing, fraud monitoring, and compliance checks, where automation can reduce delays and manual review.

- Treat infrastructure as the product. Invest in the engineering underneath real-time payments and embedded finance, including fraud detection and reconciliation pipelines, so new products can launch faster without rebuilding core systems.

- Build in compliance from day one. Design systems that produce audit trails and explainable decisions by default, so regulatory reviews speed up instead of stalling product launches.

- Make data the foundation. Unify customer and transaction data so risk scoring and personalization run on the same source of truth, paired with a business intelligence strategy that turns the data into decisions.

None of these priorities is a single technology to buy. Each is a capability to build, which is why the top fintech trends 2026 favor organizations with the engineering depth to operationalize them well.

The Future of FinTech Will Be Built Through Execution

The latest trends in fintech point to the same conclusion. The sector has matured, capital has grown selective, and the gap between the companies that scale and the ones that stall now comes down to execution. AI, embedded finance, real-time payments, open finance, RegTech, and customer experience are connected shifts in how financial services are built and delivered, and each one rewards reliable engineering over bold announcements.

For decision-makers, the practical work of the next two years is turning these fintech trends 2026 into reliable products, more efficient operations, and high-quality customer experiences. This is where Beetroot supports fintech and financial services teams as a custom engineering partner. Whether you are scaling AI into core operations or planning your next technology investment, we can help you decide where to focus.

FAQs

What are the biggest fintech trends in 2026?

The biggest fintech trends in 2026 are AI moving into core financial operations, embedded finance expanding into more customer journeys, real-time payments becoming a competitive baseline, the shift from open banking to open finance, technology-led compliance and RegTech, and customer experience becoming a stronger differentiator.

How is AI changing the future of fintech?

AI is changing the future of fintech by moving from isolated experiments into core financial operations such as underwriting, compliance, fraud detection, and customer support. The largest value comes when AI is connected to real workflows, governed data, and human oversight rather than used as a standalone tool.

Which fintech trends are driving the most growth?

The fintech trends driving the most growth are AI-enabled operations, embedded finance, and real-time payments, because each trend connects directly to revenue and efficiency. Growth increasingly favors companies that turn these trends into dependable products and operational workflows rather than pilots.

What role does open finance play in the future of financial services?

Open finance extends open banking by letting consumers securely share data across their entire financial life, including savings, investments, pensions, and insurance. This broader data sharing can support more accurate credit assessment, holistic financial dashboards, and easier switching between providers, although regulatory timelines vary by market.

Which fintech investments should companies prioritize in 2026 and 2027?

Companies should prioritize fintech investments that build durable capabilities: AI applied to operational workflows, reliable infrastructure for real-time payments and embedded finance, compliance built into core systems, and clean, connected data for personalization and risk scoring. The common principle is that returns in 2026 and 2027 favor execution and engineering depth, so investment should focus on operationalizing trends.

Subscribe to blog updates

Get the best new articles in your inbox. Get the lastest content first.

Recent articles from our magazine

Contact Us

Find out how we can help extend your tech team for sustainable growth.